Tow truck operators, auto repair shops, property managers, and everyday commuters rely on reliable coverage to keep wheels turning when mishaps occur. Insurance costs for tow trucks vary widely, reflecting vehicle type, usage patterns, and the level of protection chosen. While a basic policy may sit in the low thousands annually, more comprehensive coverage for heavier wreckers or high-risk routes can push premiums above five figures for a fleet. The following chapters unpack the cost landscape: first, a baseline view of typical cost ranges and essential coverage; second, the pricing levers insurers weigh—vehicle class, driving history, coverage limits, location, and training; and third, practical steps for shopping quotes, with guidance on major providers such as Progressive Commercial and The Hartford. By understanding how each factor influences price, everyday drivers and shop owners can ask the right questions, compare apples to apples, and build a policy that protects operations without breaking the bank.

Tow Truck Insurance Costs Demystified: Reading the Fine Print to Protect Your Fleet

Insurance costs for tow trucks sit at the intersection of risk, equipment value, and the realities of a demanding operating environment. For owners and operators who rely on tow and recovery services to keep roads moving, understanding how premiums are built is essential not only for budgeting, but also for designing a safer, more cost-efficient operation. This chapter threads together what the data show about baseline pricing, how the coverage mix shifts the total, and what actions fleets can take to manage costs without sacrificing essential protection. It begins with a perspective on baselines and moves through the factors that push premiums up or down, ending with practical guidance on quotes, risk management, and strategic planning that align insurance with the everyday realities of towing work. In the end, the goal is to translate abstract numbers into a workable plan that supports steady growth rather than a sudden financial shock when a policy renewal arrives.

At its core, tow truck insurance is about mitigating the consequences of a high-stakes business. A single tow truck operates at the sharp end of the street where collisions, roadside incidents, and loaded vehicles intersect with busy traffic, unpredictable weather, and the pressure to move quickly. That mix of exposure drives premiums higher than what many small businesses expect when they first compare general business coverage. Yet the same logic that makes premiums rise—higher potential losses, larger repair bills, and more liability exposure—also creates a path to smarter pricing through disciplined risk management, tailored coverage, and thoughtful plan design. The numbers that appear in pricing guides and insurer brochures are not random; they reflect how insurers evaluate the specific risks of tow operations, how much protection a policy includes, and how much value the insured places on risk transfer through deductibles and limits.

A common starting point in the literature on tow truck liability and auto coverage is the baseline cost for a simple, limited policy. When a business seeks only the minimum required liability and a basic level of auto protection, the price tends to be modest relative to more expansive packages. Across many regions, general liability coverage for a towing company typically lands in the low thousands per year, while commercial auto coverage for a single tow vehicle adds a few thousand more. When those numbers are added up, a basic, entry level package commonly lands somewhere in the range of a couple thousand dollars annually. This baseline is not a ceiling, but a foundation from which coverage levels and fleet size push the total higher. As with any insurance decision, the actual price depends on the specifics of the operation, the vehicles involved, and the exposure profile of the fleet.

The real-world range widens considerably once we move beyond the most fundamental protections. A small fleet with several light to mid weight tow trucks, each with liability, a modest amount of physical damage, and some protective add-ons, often sees premiums in a broader band. In some markets, a single tow truck with a basic baseline package can cost a couple thousand dollars per year, but as coverage becomes more comprehensive—adding garage liability, hired auto liability, non owned auto liability, and a robust physical damage policy—the annual cost for that same vehicle climbs noticeably. The effect of coverage scope is real and cumulative. The more you layer onto the policy, the more the premium reflects the broader protection, the greater the potential for defense against large or multiple loss events, and the higher the price tag. For fleets that want to lock in predictability, this can translate into a trade-off: pay more for certainty, or accept a leaner policy with potentially greater out-of-pocket exposure in a claim scenario.

Numbers reported by industry sources illustrate the spectrum in clear terms. A single tow truck can incur an annual cost that ranges from roughly two thousand dollars to eight thousand dollars or more for an all-in policy that covers liability, physical damage, and the core auto and garage risks associated with towing. In a broader sense, smaller operations negotiating baseline general liability and commercial auto coverage may see combined per-vehicle costs in the mid to upper thousands when modest deductibles and standard limits apply. When fleets grow or when the vehicles become specialized, the price can escalate quickly, with premium bands that rival or exceed what a single passenger vehicle owner might pay for personal coverage—yet the dollars spent are directed toward protection for higher risk, higher value equipment, and greater liability potential in roadside environments. For operators who maintain a small but active fleet, it is common to hear about total annual costs in the range of several thousand dollars per vehicle, climbing as the coverage array expands or the equipment becomes more expensive.

Two qualitative themes consistently appear in pricing discussions and policy documents. First, vehicle type and usage pattern matter a great deal. Heavy-duty rotators and high capacity wreckers, with their sophisticated booms and specialized hydraulics, carry higher replacement costs and a greater likelihood of complex loss scenarios. Insurers price these machines with corresponding premium adjustments to reflect the higher potential repair costs, the longer downtime, and the elevated risk of damage to other property during recovery operations. Conversely, smaller, lighter tow trucks are typically less expensive to insure, all else equal, because their value and exposure tend to be lower.

Second, the way the business operates shapes the risk profile. A company that runs in high-traffic urban environments, where incidents cluster and claim frequency is higher, will generally see higher premiums than a rural operation with less daily exposure. The number of vehicles, the annual mileage, and the driver roster all contribute to the estimate of expected losses. A fleet that emphasizes safety training, uses newer or safer equipment, and maintains a clean claims history often secures more favorable pricing through discounts or credits. This is not magic; it is the insurer translating on-the-ground risk management into a measurable reduction in expected losses, which in turn reduces the amount of money the insurer must reserve against future claims. In practical terms, investing in driver training, upgraded safety equipment, and meticulous fleet maintenance can produce meaningful premium reductions over time.

The scope of coverage also has a direct and sizable impact on cost. A basic policy that covers only the essentials will be cheaper than a package that includes physical damage protection, garage liability, hired auto liability, non-owned auto liability, cargo, and workers compensation. The more risk you transfer to the insurer—whether through liability limits, higher physical damage deductibles, or broader coverage extensions—the more premium you should expect to pay. Deductibles play a critical role here. A higher deductible reduces monthly or annual premium, but it increases the out-of-pocket cost if a claim occurs. The decision about deductible levels is a balancing act: smaller deductibles deliver more immediate financial protection in the event of a loss but at a higher ongoing cost; larger deductibles save premium dollars but require readiness to absorb a larger share of a potential claim. The right choice depends on the fleet’s cash flow, risk tolerance, and the financial resilience of the business.

In evaluating a policy, it is important to distinguish between on-hook towing coverage and lift or flatbed operations. On-hook towing, the scenario in which a tow truck hooks onto a vehicle and moves it without lifting, is typically less expensive to insure as a standalone risk than lift or flatbed operations, which involve higher loading risks and greater potential for vehicle damage during the loading and unloading process. This distinction matters because it informs not just the insurance price but also the structure of the policy and the types of claims most likely to arise. For operators whose business includes a mix of services, insurers will look closely at how often each service type is performed and under what conditions, and pricing will reflect the composite risk.

Beyond the coverage structure itself, the price is shaped by driver qualifications and safety culture. Experienced, certified drivers with clean records often qualify for favorable rates. This is a reminder that the human element of the business—training programs, adherence to safety protocols, and a proactive attitude toward risk management—does more than reduce the chance of an accident. It also signals to insurers that the operator is diligent about prevention, which translates into fewer and less severe claims. In this sense, investing in ongoing training and regular safety audits can yield dividends over multiple policy cycles. The result is not merely a lower premium but a lower risk exposure that makes the operation more resilient and better positioned to weather economic and operational fluctuations.

From a budgeting and planning perspective, a practical way to think about these costs is to separate the baseline price from the price of added protections. The baseline generally captures general liability and core auto coverage—elements designed to protect against third-party claims and damage to the tow vehicle itself. The additional protection pages, which often include garage liability, hired auto liability, non-owned auto liability, cargo, and workers compensation, reflect the broader risk landscape that accompanies towing operations, including the possibility of damage to a customer’s vehicle at the tow yard and the risk posed by employees using personal vehicles for work. In the aggregate, the baseline may be manageable for a small outfit, but as a fleet scales and as the business model expands to include more specialized services, the premium grows because the risk envelope grows too.

For readers curious about the practicalities of cost, a quick mental model helps. Imagine a small tow business with a handful of light-duty units that operate in suburban or smaller urban areas. A reasonable annual outlay might be in the mid to upper thousands per vehicle for a solid mix of liability and auto coverage, plus modest protections against common exposure scenarios. As the fleet expands or the operation embraces more complicated vehicles, a more expansive package that backs up the core business with higher liability limits and additional coverages becomes the more accurate proxy for annual risk transfer. The exact figures will vary by region, by the specific vehicles in service, and by the insurer’s assessment of historical loss experience. The objective remains consistent: align the policy design with actual operations, and calibrate coverages to protect the business without leaving money on the table.

Because price discovery is inherently local and policy-specific, the most reliable path to current numbers is to collect quotes from several specialized commercial vehicle insurers. The process requires compiling a description of the fleet, including vehicle types, age and condition, annual mileage, driver rosters, and the safety programs in place. It also benefits from documenting past losses and the fleet’s maintenance regime. With this information in hand, operators can compare apples to apples across carriers and select a package that provides the necessary protection while avoiding unnecessary overlaps. To make the process smoother, many fleets also consider bundling auto coverage with other commercial policies where appropriate, as this can yield multi-line discounts and administrative efficiencies that preserve cash flow in the face of premium changes.

The numbers and practices described above are not simply theoretical. They reflect a dynamic set of market conditions and regulatory environments that can push premiums in one direction or another. In some states, for example, higher traffic density, theft risk, or more stringent liability requirements can elevate the baseline costs, while in others the premium pressure may be lighter due to favorable loss histories or competitive markets. This variability underscores why a real-time quote and a carefully structured policy are essential for sound budgeting and long-term risk management. For the busy owner operator, the practical path is to translate the general framework into a concrete plan: specify coverage needs, agree on realistic deductibles, emphasize driver training, and solicit quotes from multiple carriers that specialize in commercial vehicle policies for towing and recovery operations. The objective is a policy that not only protects assets and people but also supports predictable operating costs that align with revenue realities.

The journey toward a well-balanced policy inevitably touches on how pricing is presented and understood. Some operators may encounter price targets that seem high at renewal time, only to realize that the renewal reflects a broader or more accurately assessed risk profile. In contrast, others may see gradual premium reductions as their safety program earns dividends and their claims history improves. The key takeaway is not that insurance is a fixed line item but that it is a responsive measure of the business’s risk profile. By actively managing this profile—through better training, safer equipment, disciplined maintenance, and careful fleet planning—operators can influence the levers that determine price over time rather than accepting the price as a fixed fate. This approach aligns well with the broader discipline of risk management that underpins all successful commercial operations, from the smallest one-truck operation to larger fleets with sophisticated maintenance programs and dispatch protocols.

For readers seeking a quick, practical way to visualize the cost landscape, a concise overview captures the essential components without getting lost in the extremes. The baseline general liability coverage tends to be relatively affordable, especially when bundled with primary auto coverage for the vehicles. The more you layer onto the policy, the more the premium reflects the expanded protection and the enhanced risk transfer. The premium also anchors to the vehicle type and usage: rotators and heavy-duty wreckers carry higher price tags due to value and complexity; routine local towing assets generally cost less to insure than long-haul or high-mileage operations. The operational footprint—urban versus rural, fleet size, and driver experience—weights the decision toward either a lean, cost-conscious plan or a comprehensive protection package designed to withstand large or cascading losses. As you pursue quotes, consider how the policy will interact with your business plan over multiple renewal cycles and how your risk management strategy can reduce the long-term cost of risk.

To connect the dots between pricing and practice, consider exploring a consolidated view of tow truck costs and pricing on our site. It provides a snapshot of how vehicle type, usage, and coverage levels influence costs across typical scenarios, helping you frame reasonable expectations during negotiations with insurers. See the overview at this resource for a focused look at the pricing landscape: tow-truck-costs-pricing.

When it comes to policy specifics, the architecture of a tow truck insurance program generally includes several core elements. Liability insurance remains foundational, protecting against third-party claims for bodily injury and property damage. Physical damage coverage protects the tow vehicle itself against collision and non-collision perils, preserving the asset value of a capital-intensive piece of equipment. Garage liability, a distinct coverage for incidents tied to customer vehicles housed or handled by the towing operation, addresses the risk that a customer’s car could be damaged while in your care. Hired auto liability covers situations where a driver uses a personal or non-owned vehicle for company work, while non-owned auto liability protects the business when an employee operates a vehicle not owned by the company in a business context. Workers compensation responds to on-the-job injuries, a risk that is particularly salient in physically demanding tow work. Finally, a broader commercial general liability policy can supplement the narrower garage liability with additional third-party protection. Each of these components has its own cost implication, and each contributes to the overall resilience of the business against claims, regulatory scrutiny, and the cost of doing business in a volatile market.

In the end, the question what tow truck insurance costs is best answered not by a single figure but by a price pathway defined by vehicle type, operating footprint, coverage breadth, and the rigor of risk management. A schematic takeaway is that baseline protection typically represents the low end of the cost spectrum for a single unit, often in the range of the mid thousands per year when liability and core auto coverage are included. As operations scale or as the vehicle mix becomes more specialized, the price escalates, frequently into bands where comprehensive protection and higher liability limits begin to dominate the budget. The management challenge is to design a policy that aligns with the business plan, uses deductibles and limits to balance cost and protection, and leverages safety investments to unlock premium discounts where available. A disciplined approach to driver training, preventive maintenance, and fleet safety can become a meaningful lever for cost containment over time, without compromising the protection that a towing business needs when the next call comes in and the next roadside scenario unfolds.

External resources offer broader context and official guidance on the landscape of commercial vehicle insurance. For readers who want a deeper industry perspective on coverage types, pricing ranges, and consumer guidance, a respected industry association provides detailed information and state-by-state data. This resource is valuable for understanding how the market structures risk transfer and what factors regulators and insurers consider when pricing policies for tow operations. https://www.namic.org

Pricing the Heavy Lift: Unpacking Tow Truck Insurance Costs

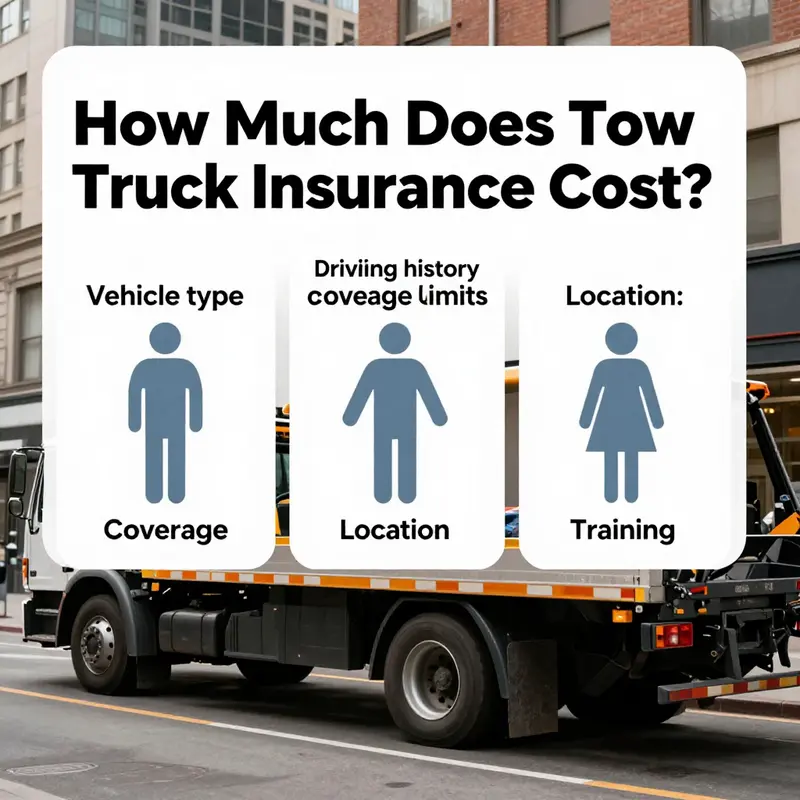

When a business sits down to price tow truck insurance, the conversation shifts from guesswork to risk calculation. Underwriters model the likelihood and cost of potential claims across a set of variables. The hull of the policy is built from the vehicle, the operators, and the surrounding operations. The premium reflects a profile of exposure drawn from five core dimensions: vehicle type, driver history, coverage, location, and training. Each dimension pushes risk in its own direction, sometimes incrementally, sometimes dramatically.\n\nThe vehicle at the center of the model is more than a metal frame. Heavy-duty wreckers, with substantial GVWR, robust hydraulics, and specialized recovery gear, carry higher replacement costs and greater potential for mechanical failure. The configuration of the tow unit—flatbed, wheel-lift, or integrated recovery apparatus—shapes the risk spectrum. A flatbed may command higher premiums when equipped with powerful winches, because of potential for on-hook damage. Smaller units can cost less to insure, but exposure hours matter. Age, maintenance, and safety features tilt risk up or down. Pricing reflects not just current equipment but how it will be used tomorrow.\n\nThe driver history is the human element in the risk equation. An operator with a clean MVR and a strong safety record tends to lower premiums, while incidents or violations raise them. CDL status signals professional standards, which may bolster confidence in safety or trigger stricter underwriting if paired with violations. Telematics and safety programs can unlock credits and shift pricing toward projected improvement. The goal is to reward safe behavior and proactive risk management rather than simply penalize past incidents.\n\nCoverage choices shape the pricing floor and ceiling. Liability coverage protects against bodily injury and property damage, often the largest premium component. Physical damage (comprehensive and collision) covers the truck and equipment. Additional coverages—on-hook/tow-in, garage-keepers, cargo—increase premium with exposure. Deductibles also influence cost: higher deductibles reduce premiums, while lower ones raise them. Endorsements and exclusions must align with contracts and regulatory requirements to avoid gaps.\n\nLocation in pricing reflects geography and market conditions. Urban areas have higher exposure hours, traffic density, and litigation risk, while rural areas may see steadier pricing. Weather, theft risk, and regulatory mandates vary by jurisdiction and affect premium calculations. Training and safety programs can drive credits, with formal curricula and documented risk reduction translating into lower costs.\n\nIn practice, a comprehensive quote emerges from collaboration between fleet managers and underwriters. A precise inventory of insured equipment, a clear usage profile, and a mapped safety program produce a transparent, apples-to-apples comparison across bids. The most effective pricing strategy blends disciplined risk management with contract-aware coverage, aligning protection with operational realities and financial goals.

null

null

Final thoughts

Understanding the cost of tow truck insurance means recognizing how vehicle type, use, coverage levels, and risk profiles interact. By starting with baseline ranges, assessing the five pricing factors, and comparing quotes from specialized providers, operators can tailor a policy that balances protection with affordability. The right coverage protects people, property, and profits, while clear shopping steps help avoid overpaying for unnecessary features.